SpaceX Stock Hit $2 Trillion on IPO Day. History Says a $10,000 Investment Will Be Worth This Much in a Year.

SpaceX just pulled off the largest IPO in history. The company priced its shares at $135 on June 12, 2026, opened at $150, and closed at $161 — a nearly 20% gain in a single session. That debut pushed SpaceX’s market capitalization above $2…

Top Real Estate Websites in USA

Finding property in the United States used to mean driving neighborhoods, calling agents, and waiting on printed listings. That world is gone. Today, the search starts online, and the platform you use shapes what you see, what you miss, and how quickly…

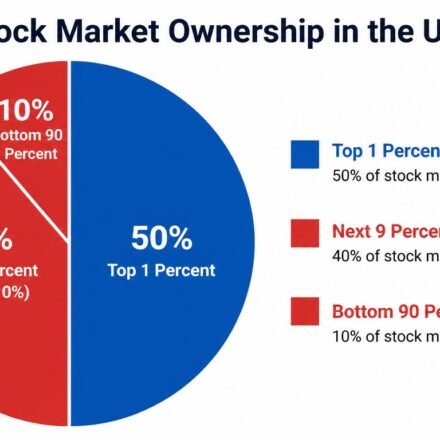

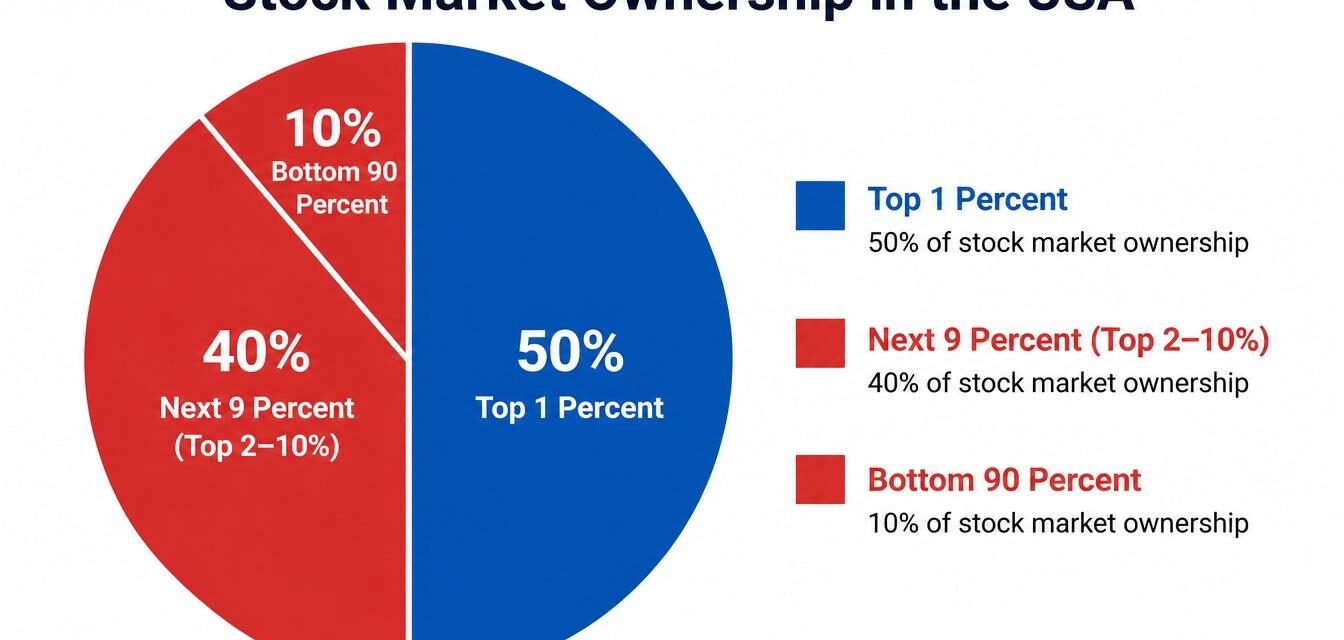

Who Owns 90% of the US Stock Market?

The US stock market is worth tens of trillions of dollars. It is the largest equity market in the world. And the ownership of that market is far more concentrated than most people realize. The top 10% of American households own approximately 90% of all…

How Much Money Should You Have Saved by Age 30?

Most people hit their late twenties and start doing the math. They look at their bank account, think about what they imagined for themselves at 22, and feel a gap. Sometimes a big one. The question of how much you should have saved by 30 is everywhere.…

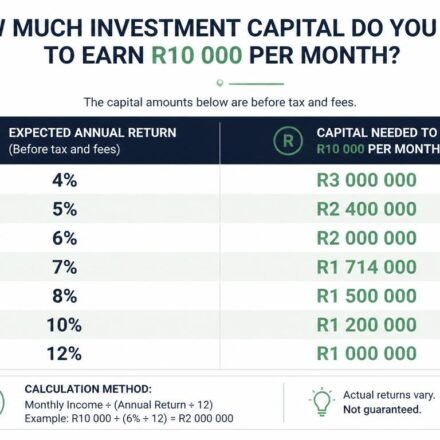

How Much Should I Invest to Get R10,000 Monthly?

This is one of the most searched questions in South African personal finance. And it makes sense. R10,000 a month is a clean, meaningful number. It covers rent in many cities. It supplements a pension. It gives a retiree breathing room. But the answer is…

Best Personal Finance Articles to Read in 2026

Why What You Read This Year Actually Matters Most people treat personal finance content like background noise. They skim a headline, feel briefly motivated, and move on without changing a single habit. That cycle is expensive. 2026 is a different kind of…

Best High-Yield Savings Accounts of 2026

Most people still have their money sitting in a standard savings account earning 0.01% interest. That is not a strategy. That is losing ground to inflation every single month. High-yield savings accounts have changed that equation significantly. In the…

Buying a Home: Mortgage Rates, Home Values & Real Estate Tips

There is a moment every serious buyer faces. You find a property that checks most of your boxes. The price feels fair. The neighborhood looks stable. Then you pull up the current mortgage rate and do the math. Suddenly the monthly payment is $400 more…

Why Is the Stock Market Moving Today?

Most days, the stock market moves for reasons that feel vague until you dig into them. Today, June 10, 2026, is not one of those days. The catalysts are clear, and they matter. Three forces are colliding at once: a fresh inflation report, a rapidly…

Personal Finance 101: Take Control of Your Money Without Stress

Money stress has a strange way of sneaking into everyday life. It shows up when you check your bank balance before payday. It happens when an unexpected bill lands in your inbox. You wonder if you are actually moving ahead financially or just running in…